The 2017 Tax Cuts and Jobs Act (TCJA) capped the State and Local Tax (SALT) deduction at $10,000 for single and joint filers ($5,000 for married individuals filing separately), making the standard deduction more attractive for many taxpayers. The One Big Beautiful Bill Act (OBBBA) raises the SALT cap to $40,000 ($20,000 for married individuals filing separately) – but with several limitations.

The deduction cap will be phased out by 30% of the excess of the taxpayer’s modified adjusted gross income (MAGI) over $500,000 ($250,000 MFS) and will return to $10,000 ($5,000 MFS) for MAGI of $600,000 ($300,000 MFS) and above. The deduction and phase-out levels will increase by 1% annually through 2029, with the cap returning to $10,000 ($5,000 MFS) in 2030. Starting in 2026, itemized deductions for those in the 37% bracket will be limited to 35% of their value. These changes mainly benefit wealthier taxpayers in high-tax states but could also lead more people to itemize deductions instead of taking the standard deduction.

In addition to SALT deductions, there are four categories of deductions taxpayers can consider claiming: medical expenses, home mortgage interest, charitable contributions, and theft and casualty losses from federally declared disasters. Some deductions, like medical expenses, have limits. For instance, only the portion of medical costs that exceeds 7.5% of your adjusted gross income (AGI) is deductible, and expenses paid through an FSA or HSA are not deductible.

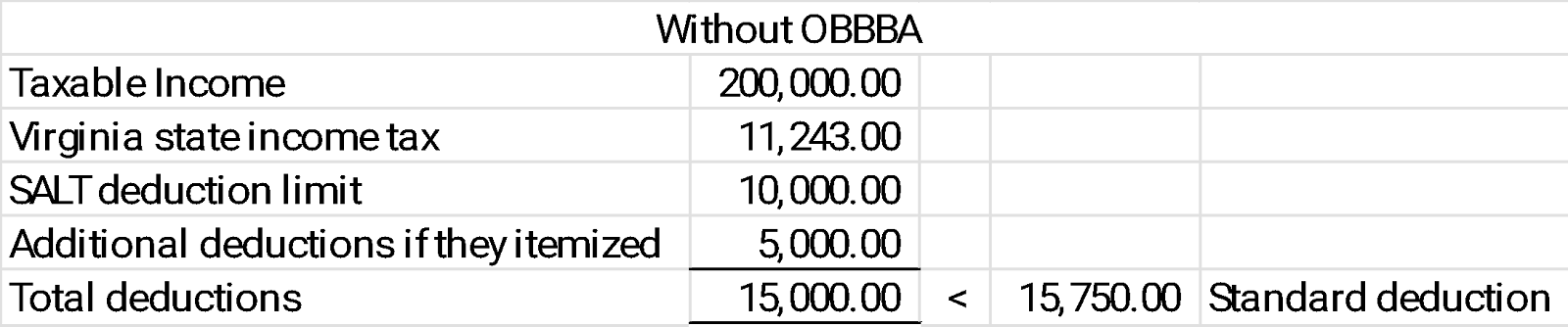

The examples below show a hypothetical single filer who lives in Virginia, earns $200,000 per year, and does not own a home. Before the OBBBA, the $10,000 SALT deduction cap would have made taking the standard deduction—$15,750 for single filers for the 2025 tax year—the better option.

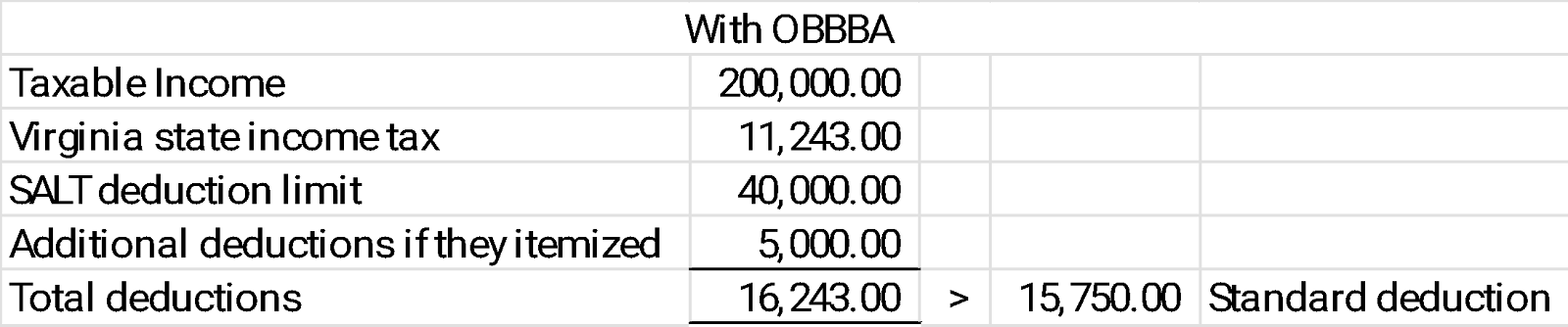

Now, with the higher SALT deduction, they might realize more tax savings by itemizing.

The hypothetical couple could potentially reduce their taxable income by an additional $493 if they itemized.

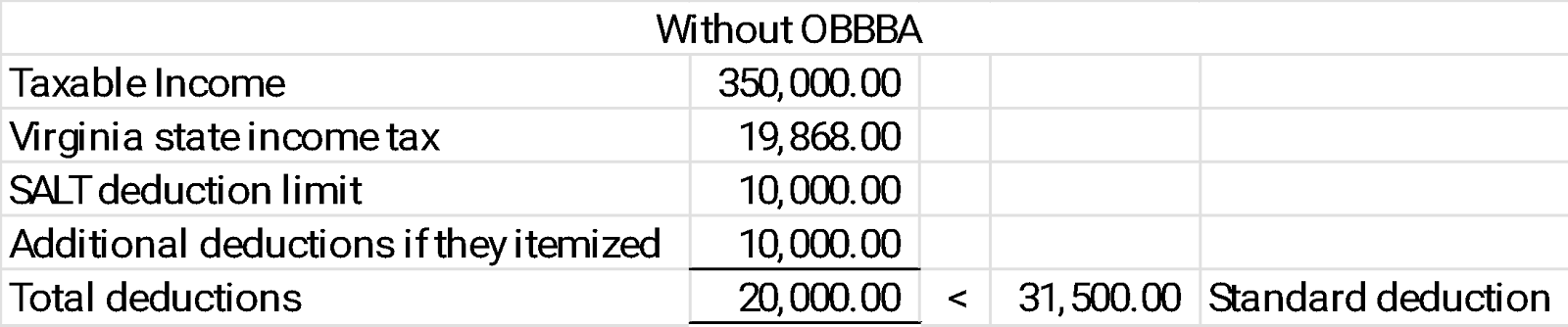

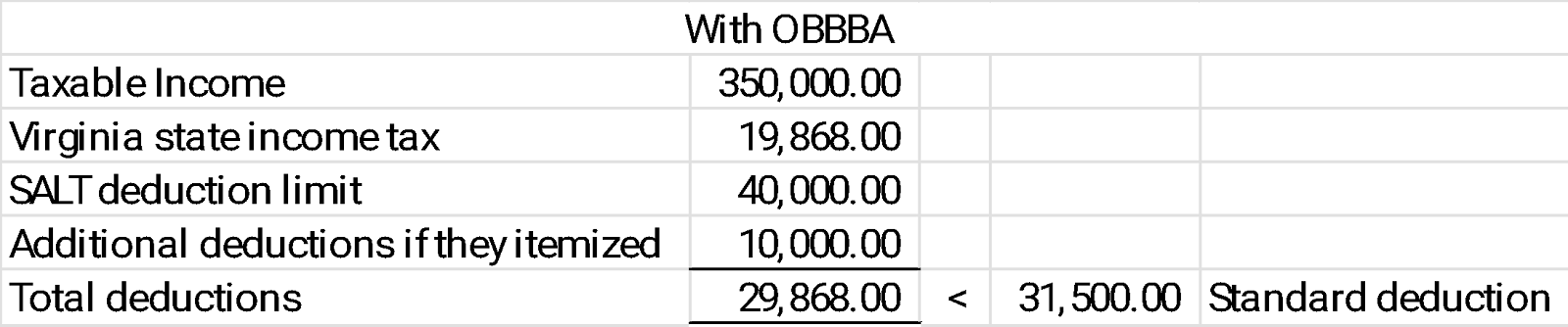

The numbers are less favorable for a hypothetical married couple filing jointly who do not own a home, as seen in the examples below. This is because single filers are eligible to claim the full $40,000 SALT deduction, while married couples filing jointly must share that amount. Moreover, unlike federal tax brackets and deductions—which typically double for married filers—state tax brackets may not increase proportionally for couples compared to single individuals.

If the couple were already itemizing—for example, because they owned a home—they would potentially benefit from the higher SALT cap like the single filer above. This holds true in all cases, as itemizing allows for additional deductions like property taxes, mortgage interest, and charitable donations.

The bottom line is, although the standard deduction may remain the better option for many, the increased SALT cap could make itemizing more appealing to a broader group of taxpayers. It may also lead to greater tax savings for those who already itemize. As you prepare your taxes this year, consider speaking with a tax or financial advisor to see how the updated SAL